Online Audit Management System

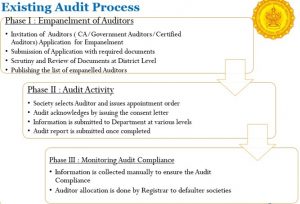

Cooperative Society Audit Process Overview:

- Department Login (DDR/AR/DJR/Commissioner):

- Auditor/Society Login:

- A good management and control of the societies in general is essential for their successful functioning.

- Auditors, therefore, act as custodian of the interests of stakeholders viz Shareholders, members, non-members, financing banks, the general public and the Government.

- Statutory Audit is mandatory every year.

- Audit is very critical activity to safeguard the interest of all the stakeholders.

- Entire Department is occupied in managing and monitoring Audit of cooperative societies.

- Manual auditing process is time consuming and inefficient resulting in lack of adherence to timely audit, less monitoring and compliance.

- On an average only 40% of cooperative societies get audited.

- Due to delay in auditing, the financial interests of stakeholders is at risk

Key Challenges :

- Redundant Efforts: Audit Information is collected at various levels leads to redundant efforts of administration. Lot of man-month efforts are wasted in coordination with stakeholders.

- No Real Time Information: Timely update is not available to administration to take appropriate action.

- Data Aggregation and Validity: Collection and aggregation of information is time consuming and inefficient.

- Poor Adherence /Compliance to Rules: Monitoring and adherence to rules is big challenge with given setup which leads to high % of defaulters among stakeholders.

- Reactive Decision making: Due to non-availability of required information in real time administration is largely works on reactive decision making.

- Spill over: Inspection and enquiry get delayed due to non/late submission of audit report/audit compliance report.

Application Objective:

- 100 % Audit Compliance of all cooperative societies across State

- To create Online repository Audit Reports

- To ensure the transparency by reducing the footfalls of stakeholders

- Reduction in Audit Defaulters year on year across the state

- Reduction in administrative efforts to ensure Audit compliance through coordination

- Reduction in paper usage.

- Efficient Administration of empaneled Auditors engaged in audit process

- Reduction in Redundant efforts

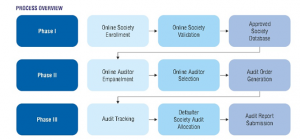

New Audit Process: